Contents

Summary

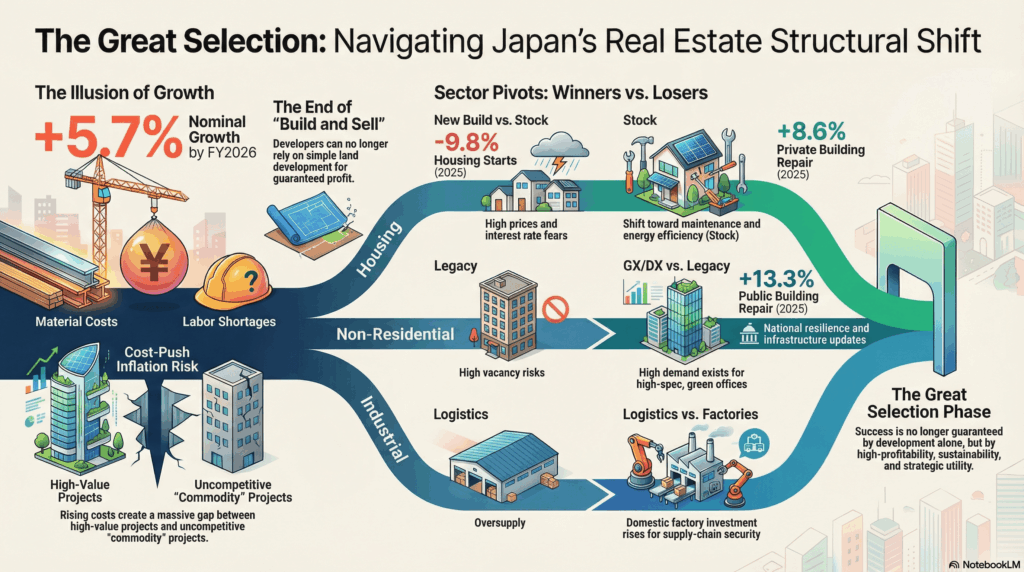

While construction investment figures in Japan are projected to rise in the coming years, this growth is largely nominal, driven by soaring material and labor costs rather than an increase in actual construction volume. The market is entering a phase of harsh selection where projects lacking high profitability will fail. A structural shift is evident in the housing sector, moving from new ownership to rental and renovation markets due to affordability issues. Meanwhile, the non-residential sector is seeing a clear polarization, with capital flowing toward domestic factories and high-specification offices, leaving uncompetitive assets behind.

High Costs Hiding Behind Investment Growth

According to the “Outlook for Construction Investment” released in January 2026, the total nominal construction investment in Japan is expected to increase by 4.7% in fiscal 2025 and 5.7% in fiscal 2026. On the surface, the market looks strong. However, it is dangerous to accept these numbers at face value.

When we look at the details, the growth in “real” value is much lower than the “nominal” value. This means the increase in investment is mostly made up of rising costs for materials and labor shortages. This is “cost-push” inflation.

For the real estate market, this means the end of the era where “if you build it, it will sell.” There is now a big gap between high-value projects that can pass these costs to tenants, and commodity projects that cannot.

Housing: From “New Build” to “Stock and Rental”

The biggest structural change is happening in the housing market. Housing starts for fiscal 2025 are predicted to drop significantly by 9.8%. While this is partly a reaction to the rush demand before new energy standards, it shows a deeper weakness in the market for new homes.

Because of high home prices and fears of rising interest rates, it is becoming very difficult for people to buy their first new home. On the other hand, demand for rental housing is strong because the number of single-person households is increasing.

Also, investment in renovation is growing fast. Private building repair investment is expected to grow by 8.6% in 2025. Money is moving from the “Flow” (new construction) market to the “Stock” (maintenance and renovation) market. The value of real estate is shifting from “being new” to “performance,” such as energy efficiency.

Non-Residential: Factories Return and Office Polarization

Investment in non-residential buildings (offices, factories, etc.) is expected to grow strongly. However, the contents of this investment are changing.

Logistics warehouses, which led the market recently, are seeing a slowdown in new starts due to oversupply fears and high costs. Instead, investment in “Factories” is increasing. This is because Japanese companies are bringing manufacturing back to Japan due to the weak yen and the need for supply chain security.

In the office market, there is a clear divide between winners and losers. There is strong demand for high-quality buildings in good locations as people return to offices. However, tenants are only willing to pay high rents for buildings with high environmental performance (GX) and digital capabilities (DX). Old buildings or those in bad locations face a high risk of losing tenants.

Public Sector Supported by “National Resilience”

Government investment continues to increase, predicted to rise by 7.8% in fiscal 2026. This is not just for economic stimulus, but for “National Resilience” against natural disasters.

A key point is that government spending on building repairs is jumping by 13.3% in 2025. Japan needs to update its old infrastructure and make public buildings energy-efficient. For construction companies, the ability to handle maintenance is becoming as important as building new things.

Adapting to a World with Interest Rates

The macro economy is slowly recovering, but inflation and financial market fluctuations remain risks.

The business model that relied on low interest rates for a long time must change. With construction costs rising and interest rates going up, only projects with high profitability can survive.

In conclusion, although the total investment numbers are rising, the Japanese market is shifting to a “High Cost, High Value” structure. The time when profit came simply from developing land is over. The winners in this market will be those who manage costs over the building’s life cycle and invest strategically in areas with real demand, such as energy saving, resilience, and domestic manufacturing.